John Batelle, one of the gurus of Search, wrote as early as 2004 that the secret of Google’s success was its understanding of the web as a database of intentions. He described the web as “a place holder for the intentions of humankind – a massive database of desires, needs, wants and likes that can be discovered, subpoenaed, archived, tracked and exploited to all sorts of ends.”

Fast-forward to the present and Batelle has observed that “web search as a pure signal has been attenuating of late – overwhelmed by the sheer magnitude of data on the web, for one, and secondly by our own increasingly complicated expectations.” Batelle goes on to speculate, quite compellingly, on other new “little signals” such as who I know (Social Graph), what I am doing (Status Update), or where I am (the Check-in) that are emerging to make sense of the “Database of Intentions”. Bing and more recently Google have introduced contextual information to their searches as a way to make more sense of the web and better meet the expectations of users. Even so, Bing and Google are still operating in a web that represents a database of intentions – and the new intentions are social and status updates.

In the business world, people are interested in different signals and so require more sophisticated search capabilities than Bing or Google. I believe the compelling “little signal” in the business world is what has changed and it is generated by the detection of what I call events, which are patterns, connections and anomalies of interest to business decision-makers. What has changed about a business and it’s market is a powerful signal. When detected by sophisticated search capabilities, it can transform the web from a database of intentions to a database of actionable business insights.

Detecting the “what has changed” signal by finding, sorting and making sense of relevant events requires a new class of search technology called intelligent business search. Intelligent business search turns the unstructured, messy, duplicative and rich content available online into an analyzable data set of business ideas, relationships, facts and trends. It derives the implied business structures of companies, industries, management, markets and the relationships that connect them. And it applies trend and anomaly detection to discern what may be emerging, unusual or material.

Intelligent business search quickly returns relevant results that can create new insights and facilitate smart, fast business decision-making. It transforms the web into an incredibly valuable database of actionable insights. Tapping into that database has the potential to transform the way you sell, market, strategically plan and think about your business.

[Posted on the Huffington Post earlier today]

We find and analyze management for our customers. It’s one of the most popular things we do. So we know that helping users get a better, richer picture of who matters in the companies and markets they care about is valuable intelligence.

Enter from stage left: Salesforce.com buys Jigsaw.com today.

Jigsaw has a mixed reputation – from Michael Arrington of Techcrunch originally calling them evil in 2006, and then in 2009 just calling them amoral – to the New York Times describing them as driven by users self interest. They’ve been growing, but not like LinkedIn; revenue has been doubling, but was it enough to go it alone? But whatever you may think about their business model, and your “friends” revealing your contact information into a central database, the net result is more than 1.2 million members and more than 22 million contacts.

Salesforce has positioned this as entering the $3B data services market – and creating “new opportunities” to partner more closely with other data providers like D&B, Hoovers and Lexis Nexis. But I think this is a classic misdirect. I agree with Michael Maoz – what’s really going on here is the convergence in the needs of CRM and the social process.

Users want dynamic, current data. They know that today the most up-to-date information is on the web. It’s in networks, it’s in blogs, it’s living in the thousands of phoenixes (or should that be the correct Latin phoenices?) rising from the ashes of the breakdown of traditional journalism. They don’t want to get data from databases built from manual processes and filings – they are simply always out of date.

And so for Salesforce, the ability to pick up a dynamic contact list and the continuously updating process behind it (since we have to assume LinkedIn was not for sale) is a way for them to bring that dynamism into their CRM platform and into their moves into social media. It’s a smart move. But I do wonder what the long term impact is for the traditional, static databases. I know at FirstRain we are replacing Factiva today because our intelligence is richer, fresher (and easier, but that’s another story) – will Salesforce end up competing with Hoovers et al?

A warning tremor rippled through the telco business last week – did you notice it? Apple announced that it will now allow iPhone users to use Internet calling services over cellular networks. Up until now you could use VoIP but only through Wi-Fi, i.e. not in most of the places you’d like make a phone call.

Last week “Apple … confirmed the change and said it applies to applications for the iPhone and the new iPad tablet device unveiled this week, some of which will come with 3G capabilities”.

You may remember that not long ago Apple blocked Google Voice which then triggered an FCC inquiry. Now “FCC Chairman Julius Genachowski on Thursday praised Apple’s latest decision”.

This is just the beginning of a disruption that will eat away at the core calling businesses of AT&T and it’s competitors. iPhone 3G apps from VoIP providers like fring, iCall and a soon to be upgraded Skype will start to eat away at call time and, while there are some technology challenges that are still annoying today, it’s only a matter of time.

Like many other technology trends it’s starting small but the disruption will be long term and profound. If your customers are in this space, or you invest in this space, there is a How To on our support blog you can use to get FirstRain to watch this space for you.

There is a fundamental change already underway in the world of books and it just accelerated yesterday. I don’t know whether to be happy to sad.

I have a Kindle. I love it, but I know I am a bit of a geek. To me, evidence that the world of books was shifting forever came when my mother (who is over 70 but how much over is private!) stated that she wanted a Kindle. And then yesterday Steve Jobs announced the iPad which has my kids friends all a’twitter (actually a’texting would be more accurate since Twitter is for old people) about ebooks now.

A couple of days ago I starting researching Amazon in FirstRain and, thinking about this phenomenon, went hunting for interesting content. As with most of our users, I tend to read certain sources and types of content more than others because of I believe they have better insight and are more reliable. FirstRain helps me sort through the noise easily by choosing the content type or sources I want to read. By selecting blogs only, I noticed a story from November titled Amazon (AMZN): “The best is still ahead”

“Amazon announced that its Kindle e-book reader is now its most popular selling item, both in units and in dollars. That led to a big acceleration in revenue growth (28%, the fastest in five quarters), while earnings leaped 67%.”

Expectations are that the holiday season was extremely successful for Amazon as online retailers, by most accounts, took share from brick-and-mortar retailers. The economic disruptions of the past two years have actually meant an acceleration in consumers’ adoption and use of the Internet as a retail channel.

Amazon’s earnings call is today so I’ll be looking for the transcript on FirstRain tonight (I can’t take the time to listen but I will speed read it) since this change to ebooks is such a ground shift in my way of consuming books – which I do voraciously.

But Amazon has bigger plans than my reading addiction. “Amazon is no longer content to be the world’s biggest e-tailer. Its new goal is to become the world’s leading retailer. Period.”

Aside from the other markets that Amazon has aspirations to dominate, I believe the company will own the market for books, both hard copy and e-books, in the next few years. Sadly the independent bookstore will all but disappear – although maybe there is room for one large single chain for the older readers who like to walk the isles, touch and smell (Yes, one of our engineers at FirstRain actually used the word smell) the books.

From looking into this in our system, it looks like the winner here will be Barnes & Noble (BKS), but I don’t believe the company will grow organically. Over the next few years, Barnes & Noble can prosper by becoming the brick and mortar bookstore choice and Amazon and Apple will garner the rest of the market share for books with both online hard copy sales and e-book sales.

Borders is definitely in decline. It will close an estimated 240 stores during the three months ending January 31, 2010 for a total of roughly 300 Waldenbooks stores over the past 13 months, or close to 70% of all Waldenbooks outlets! Retail analysts at Davidowitz & Associates give Borders Group a 50-50 chance of survival. (Added note – right after I posted this I saw the CEO has announced he is leaving and they are cutting 10% of their corporate staff).

From the Barnes & Noble website, as of October 2009, the company operates 775 stores. However, keep in mind the number of stores Barnes & Noble had at the end of 2004 was 820 so they are also down a bit. The Chicago Sun-Times reports that analysts expect an avalanche of bookstore closings this year. A new report by Grant Thornton report says 10,000 retail stores will have closed by the end of 2009. Of that number, 400 will be bookstores, which is a 500% increase in bookstore closings over 2008.

Within large department stores like WalMart and Target, the small numbers of book titles are probably safe and books will continue to be sold in niche markets like the point-of-sale newsstands in the airport where Hudson Booksellers seems to have most of the market – unless everyone who flys gets an iPad the way everyone who flys today has a cell phone .

Sadly used bookstores will probably disappear as well as no industry undermined by its greatest partisans survives for very long. Remember when CD sales plunged after music could be downloaded? Today, we can find any used book in the World for pennies on the dollar on Amazon and on other sites. “With the Internet, nothing is ever lost. That’s the good news, and that’s the bad news” says author Wendy Lesser in a New York Times piece by David Streitfeld (12/28/08).” But would this mean when I buy a first edition as a gift (as I did for a dear friend’s 50th birthday last year) I would not be able to hold it first? Hmmm… not sure about that.

What is certain is that the earthquake for books has hit, the after shocks and still coming – the iPad being the latest – and ten years from now I will probably only be buying the really hard to find history books I read in hard copy. Everything else will be coming from the cloud… another area Amazon wants to dominate but for another post.

The three most recent Signals on FirstRain tell an interesting story:

Combine this with a look at volume of content on the web around Apple. This is a chart of web content volume for Apple – here you can see that the discussion on Apple went quiet for a while, it then heated up around the Mobile computing discussion, but despite all the considerable chatter on the much-rumored Tablet on the web, the Quattro acquisition generated an even larger spike in web content.

All signs are that 2010 is the year that marks the major transition in Mobile computing platforms. The explosion of smart phones, the rapidly growing tablet choices, ebooks etc. all free consumers from their PCs and even from their Macs.

If the new Apple “Tablet” is as sexy a product as the iPhone was (and there is no reason to believe it won’t be) – their new move will allow them to grab an interesting piece of the mobile ad market and put Apple again in a commanding position.

This is probably why the Quattro acquisition is such a hot topic on FirstRain.

I sat on a panel today at NIRI (conference for IR) today in Fort Lauderdale and the topic was the changing role of the sell-side analyst. My fellow panelists represented the differing viewpoints of independent research – and a client – but the consensus was the same. The sell-side is going through radical change.

The problem started 30 years ago with commission deregulation – the day when how much a broker was paid to trade a share of stock was no longer regulated. As you can see from Rick Hanley’s chart here — the price of a trade has dropped continuously. Trading volume and investment banking were the two sources of funding for sell-side research — for the first the price per trade has plummeted, for the second Elliot Spitzer put up a wall between IB and research — and so the business model of traditional sell-side research within the big broker dealers is broken.

The net result is, unlike in the internet bubble when sell-side analysts were rock stars, now many of them have left and either gone into the buy-side or have set up their own research firms (or retired). Howard Penney from Research Edge talked about their new independent research model – clients just subscribe to research – no trading. Rick Hanley talked about his new service for management access (and how they partner with us) and Tom Digenan from UBS was the sole representative of the customer side. I was the lone techy (in a service intensive group) but rounded out the picture with the rapidly changing toolsets that are available.

In the end after much discussion and many questions from the IR professionals on how to use the sell-side it became clear that sell-side research is here to stay – but – and this is the but of change – it’s only one piece of the puzzle and is no longer the exclusive way to get to management – so IR has to learn to work with the other independent research and technology providers.

It was also clear the sell-side is not being careful enough of their company relationships. One of the IROs in the audience (who is IRO for a major cosmetics company) told me she is so frustrated with the sell-side she is ready to cut them out. Her complaint is that she can’t get the meetings she wants, with the investors she wants, through the sell-side because, at the 11th hour, they will swap out the institutions she wants her CEO and CFO to meet with and swap in their highest trading clients: the hedge funds.

There is clearly a role for unbiased management access now.

Your average search engine user has the patience of a toddler – they expect to leverage one or a few keywords to get the answer they are expecting and they’ll only try once or twice before giving up. If the results are bad, they’re not likely to try again – you’ve lost a user, or customer.

This is a hard problem to solve when the user is a senior professional looking for business information about a competitor – or the market trend behind a stock’s movement.

FirstRain is all about only the highest quality, high precision results for professional users and a critical piece of our system behind our results is our rich Metadata library. To put it simply, Metadata is data about data; for us, it’s the information architecture that captures what the documents in our system are about – and they can be about any number of concepts drawn from the thousands we’ve modeled. They can be literal (this is about Apple Computer) or they can be crossed by any number of building blocks (this is about layoffs at Motorola in Illinois).

The base layer of FirstRain is the categorization engine that identifies and tags what an article is about – a company, a market trend, an event. Since these tags determine what users see when doing research in our system (and remember – no patience with poor results), the rules that go into identifying them need to be spot on. For example, it’s necessary to ensure a new video game launch from a company like Electronic Arts is tagged appropriately, but a blog about how to reach new levels in one of their games is ignored. A single web document may have any number of tags reflecting the content in it. The article about Electronic Arts could also mention other relevant information about competitors and partners, as well as trends like video game sales; and it’s important to identify and tag each appropriate facet.

But just tagging the data to the right topics is only half the magic. Imagine what you can do if you can also analyze the frequencies of the Metadata. Keep in mind we have millions of documents in FirstRain, each containing numerous tags telling us what it’s about and where it’s from. Go back to the Electronic Arts example: FirstRain can identify the number of times EA is mentioned in conjunction with any related topic, such as new products, or any other company. We highlight spikes in these counts for our users and so show up emerging trends in number of mentions above or below their competition. These counts can give great insight into what a company is doing, or is about to do.

By treating the Metadata as a database in itself, and analyzing it for spikes and patterns we can identify emerging trends for users that they simply could not see from even the highest quality individual search results.

The global publishing giants have declared war on the new technology generation of content distributors – but they have lost sight of what consumers value and how they want to get to the value. It’s time to separate content creators from distributors. It’s time for a new business model which requires technology understanding and leadership to develop – and one that new generation search applications like Google News and Digg for the consumer, or FirstRain for the professional investor, can sign up for to get the right news to the right people at the right price for them.

Local publications like The Boston Globe are teetering on the edge of bankruptcy, others such as The Seattle Post-Intelligencer are moving exclusively online after 146 years in print and global giants like the Associated Press and Wall Street Journal are trying to fight back. But the reality is this is too little, too late and effectively going to war with your customers is a fatal strategy as Arianna Huffington posted a few days ago.

Face it – the consumers of news have changed – dramatically. We no longer read multiple news sources on the hope that we’ll find something interesting, most of the younger of us don’t take a daily physical newspaper and as services like Facebook, Digg and Twitter have shown, we expect the most interesting news to find us. It’s not that we believe news should be free – clearly there is discovery, research and production cost, but it should be allowed to roam freely across the many channels the web enables and still maintain proper attribution.

Our customers at FirstRain have shown us over the past three years that the authoritative news is no longer only found in the WSJ, FT et al. Instead it’s media like the DailyKos, Gizmodo, Consumerist, and In the Pipeline that are increasing the size of the news market pie and creating a huge demand for such obscure, on-the-edge news. In addition, the value of each piece of news varies by who’s reading it and what they plan to do with it. What a college student reads about Apple, Inc. on an obscure blog may be informative and help him plan on his next iPhone purchase, but to a portfolio manager at a Hedge Fund, that same information may be the bit of news he’s been looking for to insert into his model and make a multimillion-dollar trading decision. In both cases the news has value but the value, the search technology to find and rank the news and the delivery model is different in each case.

The critical issue still stands though – original investigative reporting is a public service that we, as a society, cannot do without. Journalists are our educators and our whistleblowers , our eyes and ears on the ground.

The news industry needs to find a recovery path through innovation and collaboration. As Scott Karp points out in his article in Publishing 2.0, this is a technology issue that is outside the comfort zone of traditional publishers. Here are three steps the AP and its 1,500 U.S. daily newspaper members and the Newspaper Association of America (NAA) need to consider in creating a viable business model for themselves and their customers:

* Protect the original content creators: Grant original content producers the opportunity to file as nonprofits under the same laws and protections offered to the Public broadcasting companies as supported by Senator Benjamin Cardin, of MD.

* Track the content: Work with aggregators like Google News, Yahoo, MSN, as well as NYT, WSJ, and the like on developing a new HTML standard that can be inserted into the original news articles to enable the tracking of news throughout its lifecycle.

* Develop a fee-sharing business model: Work with content distributors on an appropriate fee-sharing model to enable the distribution of originally published news through the various niche channels as diverse as Google News, Bloomberg, FirstRain, and even a locally-published community paper.

These options would give content producers multiple channels to sell through, and the ability to charge a real market price based on each distributor’s reach and depth, while at the same time providing an opportunity for smaller players writing original content to distribute their content through major channels for added revenue, outside of Google Adwords.

Then the AP and NAA would create a competitive environment and a generation of startups through which news is distributed to consumers and business professionals. And better yet, this would drive the separation of content creation from distribution – and set up a long term sustainable business model which is what the publishing industry so badly needs.

Who is benefitting from a down stock market, millions of lay offs, and a depressing economy? It turns out there are pockets that are doing really well – like entertainment vendors, consumers in the market for discounted luxury goods, and global online auction websites, particularly China.

The reason is that the level of unemployment and the huge losses of personal wealth positively affect some businesses. For example, video games, consoles and accessories grew 29% in 2008 and the online game website Big Fish Games sales grew 70% — but even more than that the number of subscribers has jumped 110% since September (when the layoffs really started) and Big Fish has 30 job openings. Overall visitors to online game sites grew 30% – that’s what happens when people suddenly have a lot of time on their hands. You can read the WSJ’s take on it here.

But it’s not just gaming that’s growing. Sites that help the newly income-challenged sell their luxury goods at bargain basement prices – like Craigslist and eBay – have increased traffic. www.portero.com helps you auction off those gently used luxury goods (that your spouse told you not to buy in the first place) starting at 85% off. Of course if you want a jet, a yacht or even a Rolex you can now go to www.jameslist.com which caters to those of you looking for super high-end luxury goods.

Seriously though, the growth in auction sites is being seen globally — for example Analysys International reports that China’s C2C online retail market grew 140% in 2008 to approx $16.4 billion (U.S.) and is expected to reach $56.7 billion (U.S.) by 2011.

Looks like unemployment and the subsequent bargain hunting has a silver lining for the sites that help consumers amuse themselves and save money at the same time.

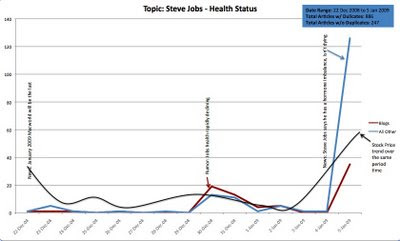

Here’s an interesting chart on the relationship between rumor, blogs, news and the stock price for Apple around Steve Job’s health . The period is Dec 22 thru Jan 5. The red line is blog volume on his ill health, the blue line is formal reported news on his health and the black curve is AAPL stock price.

Initially Apple announced that this would be the last MacWorld and that Steve would not be speaking. The stock dropped. Then Dec 30 the rumors start that Steve’s health is deteriorating. The blogs are ahead of the news and in higher volume than news, and the stock again dips. Then, when the news is official from Apple that Steve has a “hormone imbalance” (sadly no longer the whole story) the official news sites spike up, and blogs have a lower spike.

This is an example of the type of thing we see in FirstRain all the time. Blogs are ahead that something is up. They are often written by specialists with inside visibility into what’s changing – in this case people close to Apple. News follows and the stock moves on news, but that’s the same time everyone else gets the information. Most investors don’t yet have access to tools to help them sort out the junk in the blogosphere and filter for reliable sources. Queue FirstRain.

{kind=link}