Here’s another example of management turnover signalling structural changes coming in a company. The WSJ reported on Saturday that Clear Channel, the largest radio and outdoor advertising company in the US, is planning to lay off 7% of its workforce, or 1500 people. It’s behind its competitors in doing a restructuring because of the 18 month battle to take the company private which finally failed in July 2008 – but clearly management knew major layoffs were coming and started leaving.

This chart shows the detectable management departures for just the last 6 months (we pick them up from the web even though they are not announced) and compares Clear Channel with its media competitors.

I sat in on a great panel at the Web 2.0 Summit yesterday. We had executives from the health care, legal and media spaces discussing The Challenges Faced by Traditional Industries Embracing a Web 2.0 World.

I discussed FirstRain’s perspective on what we’ve seen in the financial services world. In this world the challenge in adopting a Web 2.0 platform like ours — which we’re seeing big momentum on — is working past the strong cultural bias toward established, authoritative content providers to consider Web 2.0.

Our clients typically believe that the Wall Street Journal, Financial Times, New York Times and sell-side research will cover the majority of the qualitative information that they need to know every day. Our client is also typically risk averse about their research process. It’s worked for them in many cases for 20+ years and they don’t want to change. So it takes time and effort to get them to open up to the fact that there is relevant, original, useful, and unique alternative research coming out of user-generated sources like blogs.

I also talked about the level of junk on the web and how our system removes it through a series of processes, both human and automated. My fundamental belief is that the buyside demands very high quality and that is a key to our making our customers successful.

As a panel we also talked about what had surprised us selling Web2.0 services to our traditional customers and where we thought the world was going. I discussed both the level of service our customers require, and the coming era of transparency. Both mean that we need to have a very hands on support process for our customers so that their FirstRain usage is configured both to their topic needs, and that they don’t miss anything that impacts their investment strategy.

The other panelists were all interesting, but the one I found most interesting was the GM of a Thomson division called FindLaw.com. This is a service that helps consumers find lawyers, and the most challenging thing Chris Kibarian talked about was getting lawyers to go on line. Lawyers are an inherantly conservative group and often not very tech savvy so he was very amusing describing what they go through to bring up web sites for law firms. The consumer is much more online typically than the lawyer and they’ve been delighted to see the rapid adoption of services like video and social networking within their clients web sites.

All in all – a good experience.

Per Technorati’s State of the Blogosphere Day 1 report – some fascinating statistics on who is blogging. It’s not the teenage unemployed geeks or housewives writing about their kids that the press sometimes imagines. It’s a business relevant, earning group, which is why blogs are rising so rapidly in importance as a source of news and the new wave of publishing – citizen journalism.

Did you know:

There are now a million blog posts a day – This is a huge source set of information

80% of bloggers write about brands and products – This is business relevant information

58% of bloggers are over 35 years old – The writers are mature, not kids

56% employed full time – And they are professional

51% make more than $75K/yr – And they are relatively wealthy!

And this is why the majority of our customers want us to bring blogs to the front of their FirstRain data.

Our system has been picking up an interesting counter-cyclical trend on an investment approach that has been buffered from the credit crunch recently – Sharia or Islamic compliant investing.

This is a practise that started in Malaysia three decades ago and it has been growing as the assets available have been growing in the Middle Eastern oil rich nations. New funds are being started – like the first of several new sharia-compliant hedge funds being started by Dubai based Millennium . As Reuters reports

The S&P global shariah index returned 3.61 percent in the second quarter, while the equivalent world index fell by 1.49 percent.

Banking stocks have been hammered by the credit crunch and exposure to the U.S. mortgage market. But as Islamic law prohibits the paying of interest, shariah investors — most from Gulf states which are reaping the benefit of record oil prices — cannot hold such stocks and have therefore been immune.

Guest post from Keith McCullough CEO/Chief Investment Officer at ResearchEdge

I posted on Keith’s interesting new transparency model a few days ago – here’s his thinking on the interaction of your brain and alpha in this bear market.

Mathematically speaking, “edge” is often alluded to in the investment community as “alpha”. We like alpha. Our team eats it for breakfast and washes it down with criticism and compliments alike. We know that as long as its taste remains in our bellies, we have something that will drive us toward getting up tomorrow morning.

This morning, and on those of the past few weeks, I have been waking up to increasing confirmation that we have had the “macro call” right. It’s been nine months since I left Wall Street, and while I sincerely hope that you don’t interpret my recent work as “I told you so”, I realize full well that hope is not an investment model. I have zero control over the dopamine and serotonin levels in your brain, particularly when it comes to colliding with the emotions associated with your making, saving, or losing money.

When it comes to money, the emotional impact on your brain is well researched. Richard Peterson wrote a fantastic book last year titled “Inside The Investor’s Brain – The Power Of Mind Over Money”, and I highly recommend it to anyone who is serious about trading this bear market actively. One of my favorite chapters is called “Overconfidence & Hubris”, and there you’ll find a discussion on the neurochemical balance of your investment thought processes. If you’ve already studied this, at a very basic level you know that there is a decrease in your brain’s dopamine levels at the exact time you thought you were going to be right, and weren’t. Yes, this is why some people do “dope”, it takes those worries away in the immediate term.

There is, of course, a legal solution to upping your dopamine levels – be right! As Peterson points out, “when a reward is found dopamine neurons reinforce the reward producing behavior… this is a process of learning via the dopamine pathway.” However he goes on to explain that the music of you’re being right can effectively stop, and “if a behavior is no longer rewarding, then norepinephrine levels increase in the brain. Norepinephrine stimulates scanning for new opportunities.”

These psychological facts should make perfect sense. If they don’t, you may be blessed with some Mr. Spock like “Vulcan” attributes that Peterson has some fun with. Most of us are human however, and should be very much aware that we are all going to be right and wrong over the span of an investment career. All the while, the art in making (or saving) money when others can’t lies in respecting that there are sciences at work within this complex global market ecosystem.

This morning for breakfast, as we scour the world and our respective models for those elusive “Alpha” bits, I wish you the best of luck. Our cumulative knowledge is more powerful than our individual emotions. Given that the 1st Nobel Prize in Economics was not awarded until 1969, there is plenty of creative destruction to look forward to. The evolution of investing is a process, not a point.

KM

I was struck by the juxtaposition of two articles in the last 24 hours

- Thomson Reuters plan to take share from Bloomberg and

- NYSE releasing real time quotes to the public.

Seemingly unrelated right?

Underlying both is a theme of how the ongoing trend to free content is shaping their competitive strategies and responses.

Thomson Reuters believes it can use price to take Bloomberg market share – Bloomberg being notorious for having fixed pricing and not discounting – and being expensive as a result. And the impact of free web content impacts how users view the terminals:

Neither company has sorted out a strategy for competing with online services. Michael F. Holland, the chairman of Holland & Company and the former chief executive of First Boston’s asset management division, said he can no longer justify a Bloomberg terminal for his current role and often turns to the Web for data. He first used a terminal in the 1980s and remains a fan: “There really is nothing else that’s quite like the Bloomberg,” he said. “From the beginning, it has provided incredible information. But at a very high price.”

And when asked what Google Finance and Yahoo Finance might mean for Bloomberg’s future over time, Mr. Grauer paused. “I don’t know how to answer that,” he said. “I really don’t know how to answer that.”

And John Blossom’s comment in his summary of NYSE’s move is right on:

It is, unfortunately, a familiar refrain in the content industry: major institution covets proprietary content revenues, squeezes them out for as long as possible while the markets move to find both acceptable substitutes and better ways of doing business. Publishing is in essence a very conservative business, so it’s not surprising that NYSE would try to keep this formula going for so long. But in an era when the buyers of securities have and demand information at least as good as most selling institutions failing to serve the buy side in financial markets effectively is to ignore the fundamental shift in the content industry that empowers people with independent access to content from around the world. Your content may seem safe as a proprietary asset, but if it’s not driving your clients’ profits in its most valuable user-defined contexts it is far from a safe bet in today’s content markets.

One of the technology capabilities we have in our system is looking for patterns in streams of data coming from the web. We use it to tag events, detect events and as a result pull interesting documents out of the web for our clients.

But we’re not alone in this kind of work, obviously. Wired has an article this week about how the EUs joint research team has developed the EMM: European Media Monitor which is designed to detect patterns in the stream of data.

So what patterns does EMM find? Besides sending SMS and email news alerts to eurocrats and regular people alike, EMM counts the number of stories on a given topic and looks for the names of people and places to create geotagged “clusters” for given events, like food riots in Haiti or political unrest in Zimbabwe. Burgeoning clusters and increasing numbers of stories indicate a topic of growing importance or severity. Right now EMM looks for plain old violence; project manager Erik van der Goot is tweaking the software to pick up natural and humanitarian disasters, too. “That has crisis-room applications, where you have a bunch of people trying to monitor a situation,” Van der Goot says. “We map a cluster of news reports on a screen in the front of the room — they love that.”

Clustering technology is being used in ever wider applications to find what’s interesting from the petabytes of data we now see on the web. We’re just one cool application of it, but the technology space itself is fascinating and fast paced.

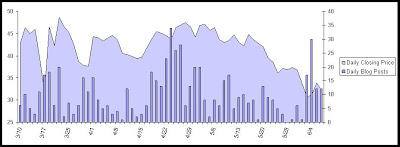

As you can see from our Blog Impact report announcement earlier this week, we’ve been watching blog frequency trends for our clients. I asked my team to do a review of Lehman’s blog stats vs. price and this is what we found. I’m no analyst so I won’t draw a direct correlation – but it is interesting to see the increase in volume of chatter before the price starts to decline and the commonality in the shape of the curves.

We’ve been doing studies of the volume of unique information on blogs and some interesting facts are coming out. With the exception of prominant tech blogs like TechCrunch, there’s a general lack of understanding/belief in the investment community about whether blogs matter or not so we’ve set out to quantify how often original and meaningful information is published on a blog first.

The challenge with blogs is that while they are exploding in volume, they are often junky and duplicative. And sometimes they are outright copies, called Splogs, designed solely to generate advertising revenue.

It takes technology, like ours, to make sense of the blog world and to identify both the quality of the source and the frequency of original posts so we can quickly identify when a unique (original) piece of information appears on a blog first (and earliest). We not only identify uniqueness, we normalize it to typical volumes by company so we can identify when a change in volume is occurring and so alert our user that there is a change in blog volume, from quality blogs, about his/her company.

When we do exhaustive analysis of blog content vs. news content, across all news sources we process (many, many thousands and far broader than retail aggregators like Google News), we see typically one new, material post per month for 80% of the large cap companies. So, if you are managing a portfolio of 100 equities, we are talking about 80 unique, meaningful pieces of information per month that you will miss – completely unacceptable for the institutional investor. And using RSS readers won’t cut it because of the level of junk and duplication – you’ll miss the one in a thousand that was different and original.